Complying with Anti Money Laundering and Countering the Financing of Terrorism Regulations of Singapore 遵守新加坡反洗钱和反恐怖主义融资条例

To comply with AML/CFT guidelines financial services firms are expected to: 为了遵守AML/CFT准则,财务服务公司应:

- Access and mitigate money laundering and terrorist financing risks; 获取和减少洗钱和恐怖主义融资风险;

- Identify and know their customers; 识别和了解他们的客户;

- Conduct regular account reviews, and 进行定期的账目审核;

- Monitor and report any suspicious transaction. 监控和报告任何可疑的交易。

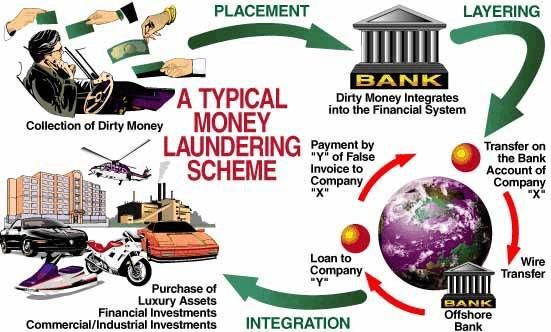

Assessing and Mitigating the risks of Money Laundering (ML) and Terrorist Financing (TF) 评估和减轻洗钱(ML)和恐怖主义融资(TF)的风险

Assessing risk specific guidelines 评估特定风险指引

- Identify ML and TF risks in your company. The guidelines suggest financial services companies look for common ML and TF threats that can be found in their: 识别公司的ML和TF风险。该指南建议财务服务公司寻找常见的ML和TF威胁,这些威胁可以在它们的:

- Customer base and their overseeing jurisdiction 客户基础和他们的监督权限

- Products (including products still under development) 产品(包括仍在开发中的产品)

- Delivery channels 交付渠道

- Services offered 提供的服务

- Third party data providers 第三方数据提供者

- Integrated IT systems 集成的IT系统

- Reaccess ML and TF Risks before launching new products, practices or technologies 在发布新产品、实践或技术之前,重新访问ML和TF风险

Mitigating risk specific guidelines: 减轻风险的具体指南:

- Ensure executive and the board of directors understand ML and TF risks 确保执行董事和董事会了解ML和TF风险

- Appoint a qualified chief officer in charge of AML/CFT compliance 任命一名合格的首席执行官负责反洗钱/CFT合规工作

- Create policies and procedures for screening new and existing staff 建立筛选新员工和现有员工的政策和程序

- Implement ongoing employee training programs so that staff up-to-date on AML/CFT policies and procedures. 实施持续的员工培训计划,使员工了解最新的AML/CFT政策和程序。

- Implement policies and procedures for document and data retention 执行文件和数据保存的政策和程序

Conduct Customer Due Diligence (CDD) and Know Your Customer (KYC) Procedures 进行客户尽职调查(CDD),了解客户(KYC)流程

CDD Specific guidelines: CDD具体的指导原则:

- Create a clear customer acceptance policy as well as procedures that identify the types of customers that are likely to pose a higher risk of ML and TF risk. When creating acceptance policy and procedures fintech companies should consider a customer’s: 创建一个清晰的客户接受策略,以及识别可能会导致更高的ML和TF风险的客户类型的过程。在制定验收政策和流程时,金融科技公司应该考虑客户的:

- Background 背景

- Occupation (including public or high-profile positions) 职业(包括公众或高层职位)

- Source of income and wealth 收入和财富的来源

- Country of origin and residence 原籍国和居住地

- Products they use 他们所使用的产品

- Nature and purpose of their accounts, 其账目的性质及目的,

- Nature and purpose of any linked accounts 任何相连账户的性质及用途

- Business activities 业务活动

- Obtain information that can uniquely identify the customer. Examples of uniquely identifying information include: 获取能够唯一标识客户的信息。独特识别信息的例子包括:

- Residential address 居住地址

- Registered or business address 注册地址或营业地址

- Date of birth 出生日期

- Date of incorporation 公司登记日期

- Nationality 国籍

- Place of incorporation 公司注册地

- Determine if the customer is from a jurisdiction with inadequate AML/CFT measures. The full list of high-risk jurisdictions can be found here. 确定客户是否来自没有充分反洗钱/CFT措施的司法管辖区。高风险司法管辖区的完整名单可在此找到。

- Determine if the customer is a Politically Exposed Person (PEP). Examples of PEPs include: 确定客户是否是政治敏感人士(PEP)。PEP的例子包括:

- Heads of state 国家元首

- Heads of government 国家的政府首脑

- Senior politicians 资深政治家

- Senior government official, 政府高级官员,

- Judicial or military officials 司法或军事官员

- Senior executives of state owned corporations 国有企业高管

- Important political party officials 政党要员

- Family members or close associates of a PEP 政治敏感人士的家庭成员或亲密伙伴

KYC specific guidelines: 了解客户的具体指导原则:

- Verify the identity of any customers, beneficial owners, as well as any persons acting on their behalf. Fintech companies should use reliable, independent source documents, data or information. Examples of identity verification include: 核实任何客户、受益所有人以及代表他们行事的任何人的身份。金融科技公司应该使用可靠、独立的源文件、数据或信息。身份验证的例子包括:

- Confirming the identity of the customer or the beneficial owner from an unexpired official document that bears a photograph. 从附有照片的未过期的官方文件中确认客户或受益所有人的身份。

- Confirming the date and place of birth from an official document such as a passport or birth certificate 从护照或出生证明等官方文件上确认出生日期和地点

- Confirming the validity of official documentation through an embassy official or notary 通过大使馆官员或公证人确认官方文件的有效性

- Confirming the residential address on documents such as a utility bill or tax statement 在水电账单或税单等文件上确认住址

- Create a customer profile. The MAS guidelines suggest creating customer profiles in order to understand if a customer’s transaction behavior poses a risk for ML and TF. A customer profile can include: 创建客户档案。MAS的指导方针建议创建客户档案,以了解客户的交易行为是否对ML和TF构成风险。客户资料可以包括:

- The nature of their business and business relationships 他们的业务性质和业务关系

- Expected level of activity 预期活动水平

- Types of transactions 类型的交易

- Sources of funds 资金来源

- Income 收入

- Overall wealth 整体财富

Conduct Enhanced Customer Due Diligence (EDD) when necessary 必要时进行客户尽职调查(EDD)

- Conduct required enhanced due diligence for customers who have been identified as higher-risk for ML and FT. Example of scenarios that require EDD include: 对于被确定为ML和FT风险较高的客户,需要加强尽职调查。需要EDD的场景包括:

- Politically Exposed Persons 有政治风险的人

- Customers from jurisdictions with inadequate AML/CFT standards 来自反洗钱/CFT标准不完善的司法管辖区的客户

- Examples of Enhanced Due Diligence. Although not an exhaustive of EDD examples, the MAS guidelines suggest: 加强尽职调查的例子。虽然没有详尽的EDD例子,但MAS的指引建议:

- Requiring Senior management approval 需要高级管理层批准

- Requiring a credit reference agency search 要求查阅信贷资料服务机构的资料

- Requiring a reference from a prior bank (including banking group reference) and contact with the bank regarding the customer; 要求提供以前银行的推荐信(包括银行集团的推荐信),并就客户与银行联系;

- Requiring verification of the customer’s income sources 要求核实客户的收入来源

- Identifying the customer’s source of funds and wealth 确定客户的资金和财富来源

- Requiring a personal reference 需要个人推荐信

Conduct regular account reviews 定期审查账目

- Develop and implement clear rules on the records that must be kept for CDD and EDD on customers 在客户的CDD和EDD记录上制定和实施明确的规则

- Keep customer information up-to-date 及时更新客户信息

- Review customer deemed as a higher risk for ML and TF on a more frequent basis 更频繁地复查ML和TF风险较高的客户

- Ensure all CDD information is compliant with the PDPA 确保所有的CDD信息符合PDPA

Monitor and report any suspicious transactions 监控和报告任何可疑的交易

- Put in place and implement adequate systems and processes that scrutinise suspicious, complex, unusually large or unusual pattern of transactions. 对可疑的、复杂的、异常庞大的或异常的交易模式实施适当的系统和程序。

- Report any suspicious activity via a Suspicious Transaction Report to the Commercial Affairs Department of Singapore. 通过可疑的交易报告向新加坡商务部门报告任何可疑的活动。